How to Calculate FEOC Compliance: A Practical Guide to IRS Safe Harbor (Notice 2026-15)

For most battery storage projects, the challenge with Foreign Entity of Concern (FEOC) compliance is first to determine if the FEOC compliant cost premium is worth it and then it’s figuring out how to actually calculate it.

The recent IRS Notice 2026-15, covering projects claiming Investment Tax Credits (ITC) 45Y/48E and eligible components/production under 45X, formalized how to calculate exposure to Prohibited Foreign Entities (PFE) using a standardized framework based on existing guidelines for Domestic Content calculations, rather than leaving it to interpretation. Developers and EPCs have to determine whether their projects include “material assistance” from a FEOC, which in practice means tracing where key components are manufactured, how much of the system’s cost is tied to those sources.

For facilities and components covered by FEOC rules beginning construction in 2026 and beyond, exceeding PFE limits can fully disqualify the project or component from the tax credit. So the most immediate question becomes:

How do you actually calculate whether your project qualifies?

Understand the metric that matters — MACR

The framework centers on a single metric: Material Assistance Cost Ratio (MACR).

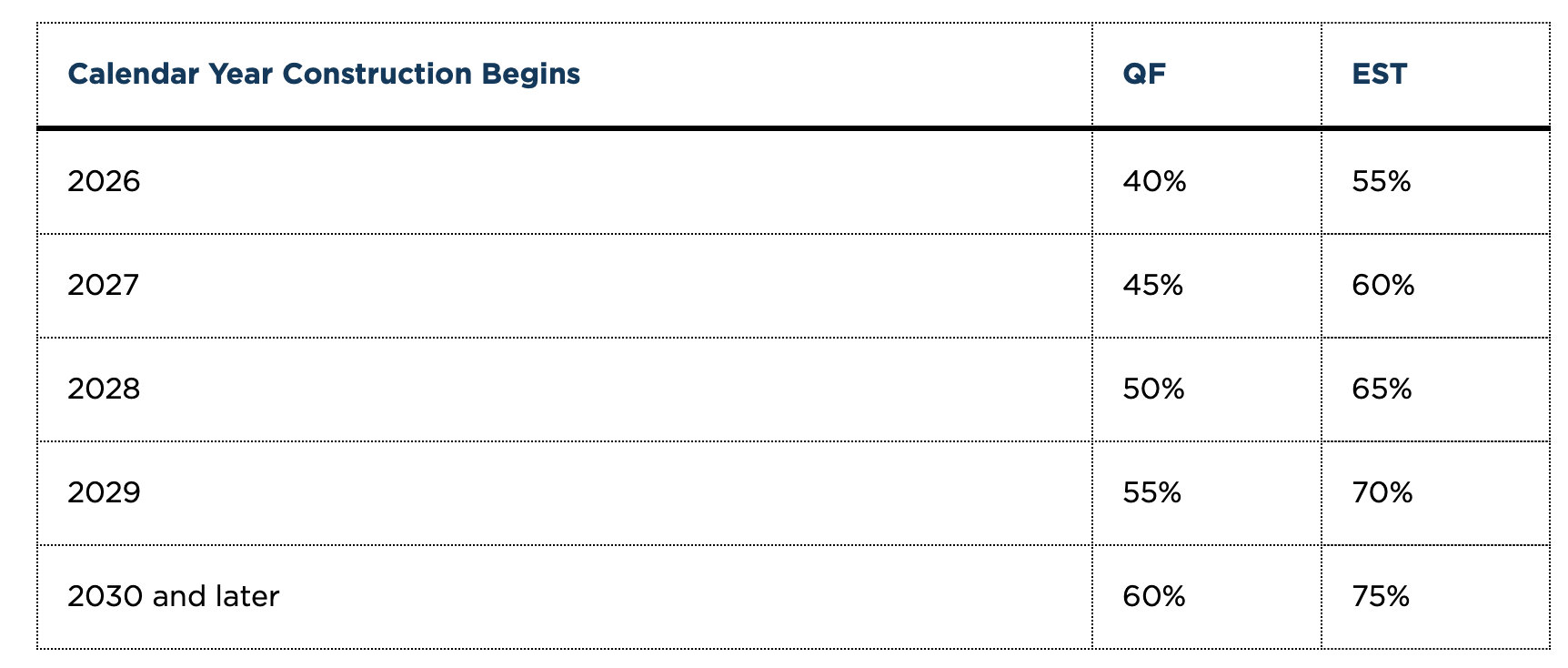

MACR measures the percentage of a project’s component costs that are not attributable to PFEs. Thresholds set by the IRS increase over time, and vary between PV / solar as ‘Qualified Facility’ (QF) vs. Energy Storage Technology (EST).

If MACR falls below the applicable threshold, the project does not qualify for the tax credit. And all of the Safe Harbor guidance ultimately feeds into how this value is calculated. If you are doing a combined PV + battery system project, you will need to calculate the MACR independently. For example, a 2026 installation year PV is 40% MACR threshold and BESS is 55% MACR threshold.

In this article, we focus on energy storage based MACR calculations.

Step 1: Choose a Safe Harbor approach

The IRS provides multiple methods for calculating MACR. In practice, two approaches are most relevant for developers.

Safe Harbor percentage cost method

Is available only if you also use the Identification Safe Harbor tables to define the components in scope, and then assign cost weight to each component

Avoids the need for actual cost accounting

Tradeoff: The method applies fixed assumptions. In battery systems, this often results in entire components being treated as PFE, even if only part of the component is sourced from a PFE.

Safe Harbor via certification & direct cost method

Relies on supplier-provided certification of non-PFE content

Uses actual cost breakdowns instead of fixed percentages

Tradeoff: This method requires supplier participation and documentation with more formal requirements (certifications under penalty of perjury, EIN disclosure, record retention) – and to be retained for at least six years.

Step 2: Apply the cost tables

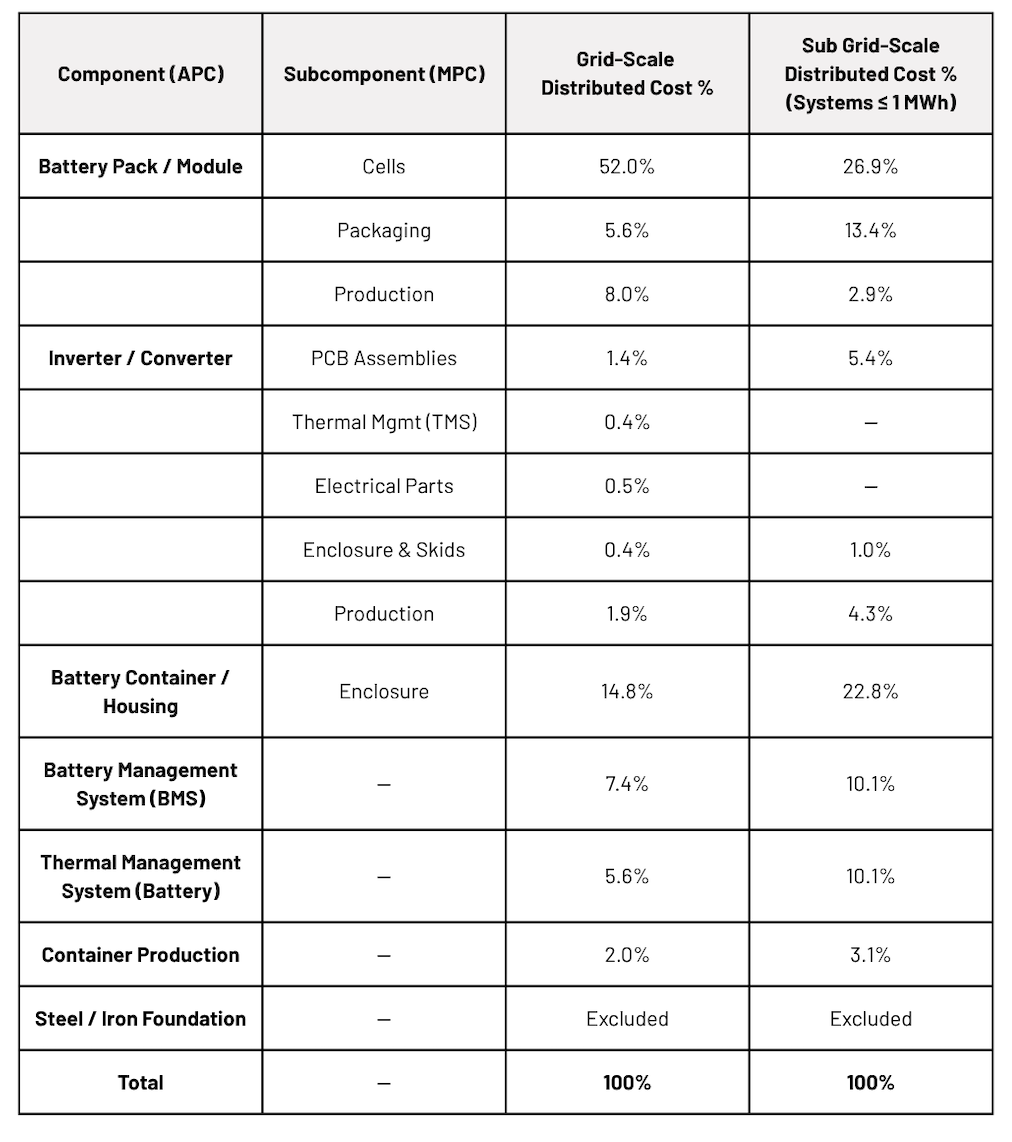

Under the cost percentage approach, the IRS assigns relative cost weight to each component in the system, see the table reference below for BESS components. The key implication is that component-level decisions do not carry equal weight.

For battery systems in particular, a small number of components can drive the majority of the calculation – particularly for larger projects (over 1 MWh). However for projects < 1 MWh, it can be easier to achieve FEOC compliance using components from PFEs.

Why BESS is sensitive to FEOC exposure

For commercial and grid-scale battery systems, cost concentration is high with battery cells. As a result, cell sourcing alone can determine whether a project meets MACR thresholds for these larger projects.

At grid scale, battery cells can account for a large portion of total system cost. The result? A single sourcing decision—where your cells come from—can determine whether your project qualifies.

Alternatively, battery cells from Korean, Japanese, and emerging American manufacturers can be a more secure pathway for FEOC compliance for projects over 1MWh.

This issue though is less pronounced in smaller, distributed systems, where cost is more evenly distributed across components, which you will see outlined in the examples below.

Practical scenarios

The following examples are simplified use cases with IRS cost tables for battery storage systems to illustrate how different sourcing decisions affect outcomes. When applying EST thresholds, most common grid-scale configurations fail without changes to cell sourcing or certification, however with < 1 MWh projects, this becomes more achievable.

Note: Smaller systems have structurally easier compliance pathways due to different cost composition.

Distributed BESS has a structurally easier path to FEOC compliance because no single component dominates the cost stack.

Critical nuances that can change outcomes

Several elements in the guidance can materially change results, here are some that caught our eye:

Separate calculations for solar and storage: Each asset must independently meet MACR thresholds

Treatment of production costs is:

Excluded if the manufacturer is a PFE (if any component is a sub-component tracing to a PFE)

Included if the manufacturer is not a PFE

In practice, if a manufacturer—or key subcomponents—fall under PFE rules, a large portion of that product’s cost will be treated as PFE‑tainted.

Steel and iron exclusion: Certain structural steel and iron items are carved out and not counted in the MACR cost base under the safe harbor tables, consistent with domestic content treatment.

Table-driven scope: Only listed and defined components in IRS tables are considered in the calculation

The difference in cost composition materially changes FEOC outcomes: In grid-scale systems, cells alone can determine pass/fail. In distributed systems, cost is spread across more components, making compliance achievable even with some PFE exposure.

What this means for the market

Notice 2026-15 does not introduce new concepts so much as it formalizes how compliance is measured, and more guidance is expected later this year.

Projects that meet the threshold retain access to the credit. Those that do not, do not. And that distinction now comes down to how the inputs are modeled.

That said, FEOC compliance is not always the optimal path. Developers still need to weigh whether the cost and constraints required to qualify for the ITC justify the benefit. We explored that decision framework in more detail here: What developers and EPCs now need from battery suppliers in the FEOC era.

Making that determination requires scenario-based analysis across sourcing strategies, timelines, and tax outcomes. This is the type of analysis GridVest supports—helping teams evaluate tradeoffs and make informed decisions before procurement is locked in.

Want to discuss?

IRS Safe Harbor Cost Table for Grid-Scale BESS

Reference: This table below reflects the IRS-assigned cost percentages for grid-scale and sub-grid scale (Systems ≤ 1 MWh) battery energy storage systems under Notice 2025-08, as referenced in Notice 2026-15. These values are used in the Cost Percentage Safe Harbor to calculate MACR.